3-2-1: We Need More Small Developers, Appraisal Anticipation, Using State Tax Credits, & More

Week #17

Happy Thanksgiving —

Here are 3 things from others, 2 things from me, and 1 picture related to incremental real estate development:

Blockhouse

We Need More Small Developers

The T-Word

Appraisal Anticipation

The Difficulties with Using State Tax Credits

The Era in Manhattan

Enjoy!

3 THINGS FROM OTHERS

I. Blockhouse

It seems like every other week that I discover the next coolest small-scale development project. Although I’m somewhat reassured by that. A lot of smart people out there are pushing the envelope on innovative housing concepts.

So here’s your bi-weekly fix—Blockhouse, a $2M 14-unit development in Spokane, WA built in 2020 on half an acre of land.

Blockhouse hosts eight residential buildings consisting of two townhouses, two duplexes, and four single-family homes. Residential units range from 480-960 SF while the Airbnb rentals clock in at 280 SF.

A few details stand out to me:

Net-zero design with a focus on sustainability. This includes rooftops lined with solar and use of cross-laminated timber made of small-diameter and sometimes diseased or dead trees

Modular construction that emphasizes efficient use of space and materials. The developers even created what they’re calling a SmartWall that contains all utilities (plumbing, electrical, data) in a single wall

Integration of short and long term rentals. The Airbnbs achieve 95% occupancy and—at $100/night—help offset the monthly costs for permanent residents

This was the first project of the 6-person development group—a testament to the power of bringing several folks with different backgrounds to the table

And the best part? It was built for $142,000 per unit, or $357/SF, all-in.

II. We Need More Small Developers

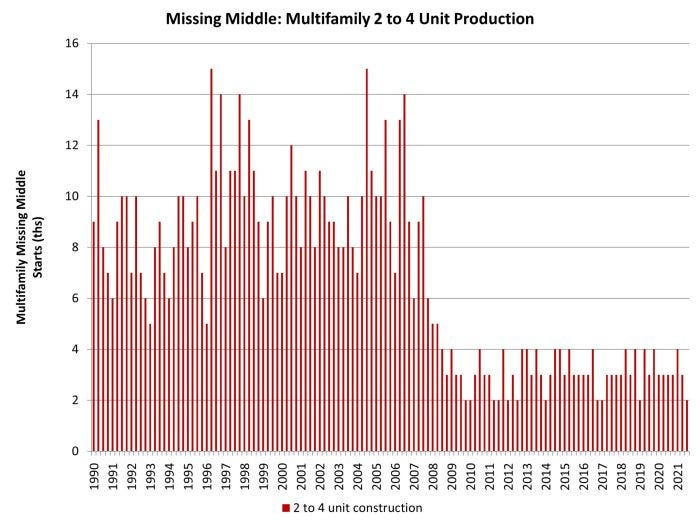

New small-scale development just can’t seem to stand up straight. Take a look at this chart of new small multi-family housing starts since 1990.

The Great Recession tanked new starts for small multi-family units by 75% and the “industry” has since flatlined at 12,000 units per year. I put industry in quotes because that’s a drop in the bucket compared to the 1M single-family homes (SFH) and 375,000 large multi-family (5+ units) residences started in 2020.

Small multi-family development is not really an industry by any standards. And it’s certainly not dominated by national players. Instead, a small army of incremental developers has taken on that responsibility—regular people motivated by making a difference in their communities.

I’m not entirely sure what has suppressed new small multi-family starts. For reference, SFH home starts have more than doubled since hitting rock bottom in 2008-2009. But if I had to wager, I’d bet it’s reflective of how small, local developers are capitalized vs national companies.

As a small developer, you take on massive individual risk—personal guarantees for debt, outlay of a large portion of net worth, leveraging your reputation to bring in investors. One failed project can sink the ship. And, in 2008, a lot of ships went down.

I’m sure a lot of small developers that were active leading up to the Great Recession have some deep scars. Scars that have deterred them from starting any or many new projects in the aftermath. Contrast that to the national builders who are well on their way to recovering from their temporary hiatuses (those that didn’t go belly up, that is).

If anything, the data above only reinforces the need for more Missing Middle housing. And it points to the need for us to encourage and support more folks to take on small development projects in their communities.

For anyone interested in trying their hand at development, I’d recommend the resources that the Incremental Development Alliance offers as a good starting point.

III. The T-Word

This is exactly how I feel as I try to justify some of my acquisitions to friends, family, colleagues, investors, randos on the street, or anyone else that will listen. Too many people out there are quick to whip out the T-word (teardown or turd, either one).

How about treasure instead?

2 THINGS FROM ME

I. Appraisal Anticipation

Appraisal for 501 Main is in!

We hit another milestone this week with the post-construction appraisal coming in at $1,075,000. That’s a little over $100,000 more than what we needed to close on the $700,000 construction loan.

For the real estate investors out there, that puts us at a 7 cap for the project. And for those not as in the weeds of real estate finance, here’s a primer on cap rates and why they’re important in real estate.

Almost 16 weeks of waiting. 16 freakin’ weeks! For four months, I sat in the dark on whether the capital structure I meticulously devised would hold. The capital structure hinges on the completed value of the project, an amount that’s determined by the appraiser. Up until this point, the pro forma is really just a collection of (educated) assumptions—the first validation (of many) doesn’t occur until the appraiser submits their opinion of value.

If the appraisal had come in lower than anticipated, that would’ve been a major blow for the project. Two things would have then had to happen:

I would need to reconsider whether the project is actually feasible. If an appraiser is valuing the building lower than you are, that’s a good sign that you’ve overlooked something critical. That said, I did catch an appraiser low ball a refinance on another project last year by 20% and had to write up my own report to convince him why he was undervaluing the project. Against all odds, it actually worked. But that’s definitely the exception.

If I still thought the project was sound after revisiting the numbers, I’d then need to go back to investors and raise more money. The bank will only lend up to 75% of the appraised value so the added gap between debt funding and project costs would need to be filled by more equity. This would dilute ownership shares and lower the returns for investors. Not a great way to start off a project.

Those 16 weeks created an excruciating period of limbo. Not only because of the reasons above. This period also overlapped with the stage in the development process where the architects and engineers should have started drafting the construction set. That is, the final plans we’ll submit for permitting and construction.

This stage is where the majority of the $50,000 in architecture and engineering (A&E) costs are incurred. So you kind of slow roll the A&E while you wait to get confirmation on the appraisal because it would only add to the pain if you shell out tens of thousands of dollars for plans only to find out the project isn’t financeable. Ideally, the appraisal would have only taken a few weeks so that this overlap could all be avoided but, alas, that’s just not the world we live in now.

Regardless, that’s all moot now.

Pause for a big sigh of relief…

And now the final push begins to submit our permit application in January.

II. The Difficulties with Using State Tax Credits

State tax credits are all the rage for small development projects. Have a funding gap? Looking for ways to make your project feasible financially? Go get some state tax credits. Granted, it’s a competitive process but free money is never easy. The thing is—actually using the credits once you’ve won them is a bit more complicated than it might seem on the surface.

I shared previously that 501 Main was awarded $86,000 in state tax credits (the project even got a mention in the regional paper). The program is designed to support the revitalization of historic buildings in designated downtowns and village centers throughout Vermont.

I’ll share a bit of my ongoing experience the last few weeks figuring out how to actually use these tax credits. Because it’s not like the state just hands you a check and says bon chance.

Note: my experience is limited to Vermont’s Downtown & Village Center Tax Credit program. Every program will have different stipulations on how the credits can be used and/or sold.

Ok. So first of all, they’re state tax credits. Meaning they provide a dollar-for-dollar reduction in state tax liability. This is great if you’re a business (or person) that pays $86,000 in state taxes each year. Unfortunately, I’m nowhere close to having that problem.

Furthermore, the credits are issued only after construction is complete. We have commitment on the award now, but need to prove the work is complete before actually receiving them.

Unused credits can carry forward for nine years but that still doesn’t solve the immediate funding problem. That $86,000 is a key part of the project’s capital stack and that funding is needed during construction. We need to find some way to turn the credits into liquid capital.

Luckily, our state tax credits can be sold to any business that has the appetite to use them. Typically, that’s a bank or insurance company.

The solution to the liquidity issue is actually two-part:

Find an institution to sell to and get them to provide a commitment letter to purchase once construction is complete and the tax credits are issued

Find a lender to provide a bridge loan secured by the above institution’s commitment letter. This will provide the liquidity to use the tax credit award during construction

Believe it or not, this isn’t some backdoor hustle I just came up with. It’s actually standard practice, especially for smaller developers that rely on the credits for construction expenses.

In theory, you would try to bundle the tax credit purchase and bridge loan with the construction financing so that a single bank is handling the whole burrito. I was late to the fiesta, though, and found out only after we had secured a commitment on the construction loan that the lender had zero interest in getting involved with tax credits.

As it turns out, there aren’t many institutions that are interested in purchasing and lending on such a small tax credit. It’s almost too much of a pain for them to make it worth their while. So I’ve spent the last few weeks reaching out to and speaking with 10+ institutions and, of those, I landed one lead on a tangible solution.

But one is all you really need to make it work.

Fortunately, I found a bank that will both purchase and provide a bridge loan. The downside is that they’ll only pay $.90 on the dollar while also tacking on a 5% interest rate to the bridge loan. Meaning we’ll only actually be able to capture around $73,500 of the actual $86,000 award.

That’s $12,500 lost right off the bat. I won’t pretend to understand the state’s economic rationale for structuring the award as a tax credit but I will say that it is inefficient. Why not make the award a grant? The state could continue to issue the awards following project completion to avoid fraud while still necessitating a bridge loan. But at least the recipient could avoid paying 10% to an institution that acts like they’re doing us a favor by taking the credit off our hands.

Don’t get me wrong. It’s a great program as-is. It’s impossible to complain about free money. And plenty of impactful projects would go unfunded if the program didn’t exist, including 501 Main.

But if the goal is truly downtown revitalization and the state is issuing $5M of these awards per year, then ~$500,000 of that is going straight to the bottom line of large institutions. Or, the equivalent of six 501 Main projects that could have been funded if the program were structured more efficiently and didn’t require skimming 10% off the top.

1 PICTURE

I.

I know this new condo factory is the antithesis of incremental development but I kind of like it. Sure it’s showy and far from affordable. But it’s so precarious that it warrants awe from an engineering perspective alone.

📍 The Era in Manhattan, NYC

That’s it for today. Thanks for reading. If you haven’t yet, go ahead and subscribe here:

About me: I’m Jonah Richard, a small-scale real estate developer in Vermont. With my company, Village Ventures, I’m currently getting my hands dirty redeveloping mixed-use buildings along Main Street while trying to pick apart and replicate what makes other communities thrive.

Want to learn more about my projects and incremental real estate development? Connect with me on LinkedIn, Instagram, or Twitter.

I was an accountant when the 2008 recession hit, and while it hurt a lot of small builders, a lot were my age close enough to retirement that they just retired. The other item that I have not seen elsewhere was cost of insurance for the builders. It increased from 500% to 1000% after 2008, killing many of the small builders that survived 2008.