How One Construction Draw Almost Cost Me $10,000

How One Construction Draw Almost Cost Me $10,000

A lesson in construction loans and working capital.

Hey. Welcome to the next edition of Small-Scale Sunday from Brick + Mortar where small-scale developers get actionable tips on acquisition, financing, design, construction, and operations.

As a disclaimer, this isn’t a blitz at my lender.

They’ve actually been very accommodating and pleasant to work with—two adjectives rarely used alongside “lender”.

The lesson here is more about managing funds as a smaller developer.

Specifically, I want to show you a costly trap I almost fell into that you can avoid with the right planning.

First, let’s define a few terms:

A draw is the funds released from your construction loan by your lender

A distribution request is the packet you send your lender to initiate a draw. This includes notarized request forms, a construction budget tracker, contractor lien waivers, & more

Working capital is the money you have in your bank readily available to pay subs, buy materials, cover holding costs, etc

As working capital gets low, you submit a distribution request for more money (the draw).

Ok. Storytime.

I closed on my construction loan for 501 Main in January. At the time, my lender requested I wire them all equity funds to retain and administer.

Naively, I obliged.

This meant that, when the project started in March, I had no funds in the account to buy materials or pay subs. And draws can only be made for expenses incurred retroactively.

Fortunately, I had already spent $50,000 on soft costs before closing the loan (architecture and engineering) and I immediately submitted a distribution request for that amount.

The draw was processed quickly and this $50,000 became my working capital.

$50,000 roughly translates to one month of working capital—the average sum I spend each month on project expenses.

And this worked for the first few months.

At the beginning of each month (once all prior month’s invoices were received and paid), I submitted a distribution request for the amount spent. My lender would pay out the draw a few days later and that would replenish my working capital.

My monthly expenses were mostly split between two vendors during that period:

The local building supplier where I purchase most materials. Invoices are released on the 1st of month and due on 10th to be eligible for a 10% discount (average $30k/mo in spend)

The carpentry crew framing the building. Invoices are paid every Friday (average $15k/mo)

Then, last month, we hit 25% project completion.

This triggered a 3rd party audit—a process where the lender hires a consultant to analyze expenses incurred, do a walkthrough of the project, and prepare a formal report.

Although slow, the audit serves as a safety precaution to both prevent fraud and identify areas at risk of going over budget.

There’s no question as to the value this provides the lender.

But watch how this unfolds for me…

…me, the sucker with only one month of working capital.

June 1st rolls around. And in comes the May statement from the building supplier for $41,000. But hold up. I only have $20,000 of working capital left in the bank after paying subs throughout May.

Time to prepare a distribution request.

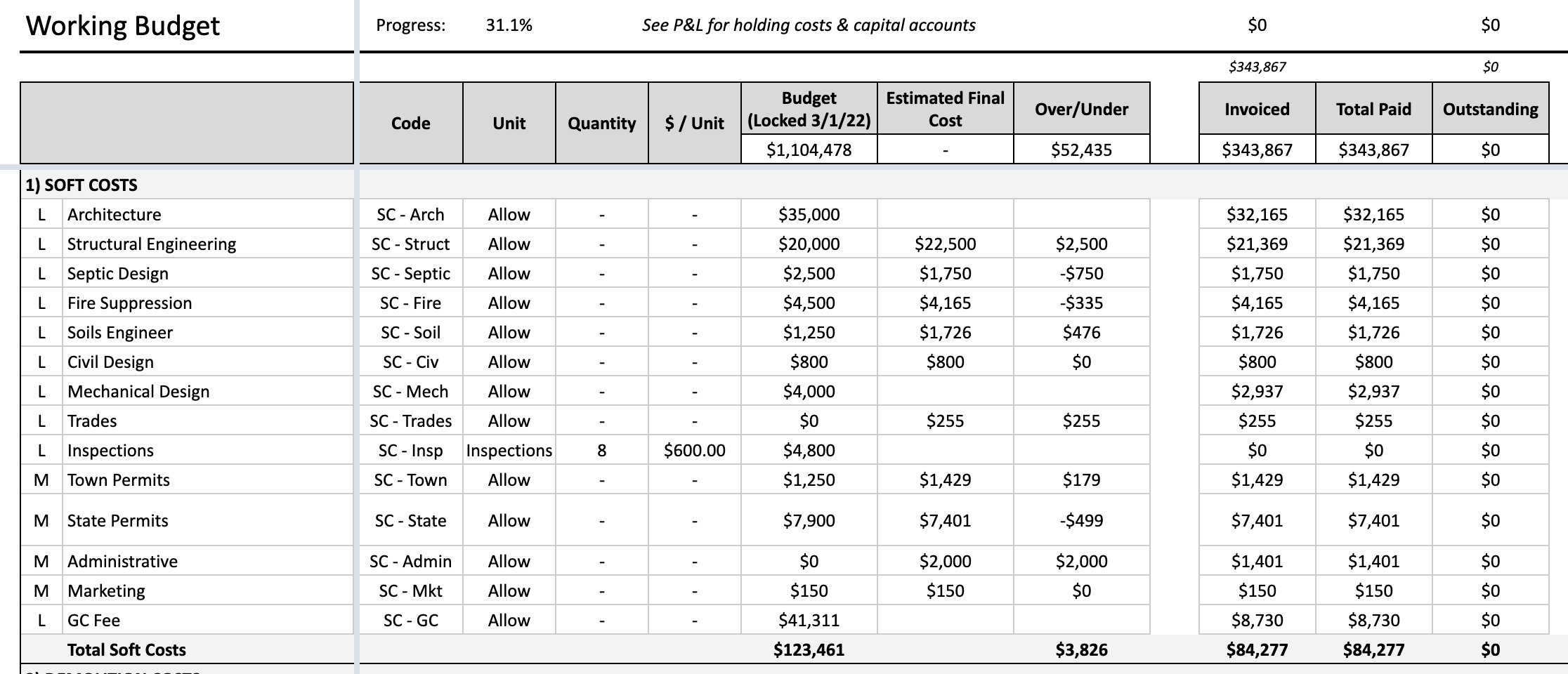

It takes me a few days to pull these together. Administratively, they’re a headache (although, to be fair, all administrative work is a headache). Every purchase is manually entered into a tracker that reports how we’re holding up against the initial budget projections. I do this across 150+ categories.

This tracker is something I came up with (send me an email if you want a copy).

Regardless, the lender has their own version. One with broader categories (e.g. soft costs or framing). Whether you like it or not, some level of manual data entry is required. I just go one step further because I want the data for future projects.

June 6: I submit the distribution request to my lender. They then initiate the 3rd-party audit.

By June 10th, it is clear that the disbursement will take time. So, to avoid losing out on the 10% discount from the building supplier, I put the $37,000 invoice (90% of $41,000) on my credit card.

A week goes by. Then, the site visit happens. The auditor is in and out within 15 minutes (plus 3 hours of round trip travel billed at $175/hr).

He takes some pictures and asks a few basic questions (“are you the GC?”; “can you tell me about the project?”).

My one takeaway was that he was impressed by the quality of the products we used. And, naturally, I extrapolated that as a compliment to the team for their craftsmanship. Because, like, who just compliments the use of TJIs and LVLs, right?

Another week goes by. The auditor asks for additional information (site plan, old lien waivers, etc). I oblige again.

And another week goes by. I check in with my lender. Turns out, the forms I had been sharing with my disbursement requests were not “industry standard.” I receive new forms to fill out (here and here if you’re curious what industry standard looks like). I clear my schedule that afternoon to complete the new forms.

But wait. Another week goes by. I’m starting to get worried. By now, it’s early July and a new $34,000 invoice from the building supplier has been issued.

I check the project bank account—$103 left. Wow. Plus a maxed out credit card. Yikes. If I don’t pay the new $34,000 invoice by the 10th, I lose out on the $3,400 discount.

Not only that, but the payment for my maxed out credit card is coming due. Or else I accrue a $750 interest charge.

Every day I check in with my lender. My hope is to make it very clear the position I’m in.

And then, voilà.

On July 6th, my draw shows up in my bank account. I scramble to pay off my credit card before the interest charge hits, then turn around and pay the July invoice from the building supplier.

Finally, the cherry on top.

I get an invoice from the auditor. $1,800. For a report that was just a copy/paste of information I provided him. Alongside a few pixelated pictures of the site. Take a look (don’t worry, it’s redacted).

In the end, this single draw almost cost:

$4,100 in lost discount from June statement

$600 in late charges from building supplier for not paying June statement by the 30th

$750 in late charges on credit card

$3,400 in lost discount from July statement

$1,800 in auditor fees

Or $10,650 total. Just to access my own money.

Instead, I was able to avoid $8,850 of that by getting a little creative with the credit card. Although I’m still in awe of the amount paid to the auditor.

It’s easy to look from the outside in and think: that’s a million dollar construction project, what does an extra $8,850 matter?

But, in that $1m budget, every penny is accounted for. And those 10% discounts from the building supplier are critical to us staying on track financially.

Yes, there’s some contingency. But that’s reserved for serious cost overruns, not artificial bloat from a routine administrative process.

So, what’s the lesson here?

Short answer:

Make sure you have enough working capital.

Two months is ideal (vs the one month I’m working with).

Project out your monthly run rate before you close on the loan and hand all your equity funds over to the lender. Then make sure you’re able to retain those two months of working capital from your equity contribution.

Maxing out your credit card as a bridge loan is not a good strategy. And not one that I would like to repeat. Although who knows—I’m stuck with one month of working capital and there are three audits left before project completion.

There’s nothing that you, as a small developer, can do about long draw cycles—it’s generally outside your control.

However, you can control how you mitigate the risk. So plan accordingly.

Over the long term, I’d love to see changes to how draws are administered for smaller projects. In bigger development shops, there are back office jobs dedicated to managing the draw process.

But for the small developer without the overhead, it’s cumbersome. And every minute (or hours in the case of managing draws) is time that could be better used on pushing the project forward—marketing units, choosing fixtures, researching systems, writing this blog (?), etc.

What changes would I like to see? That’s a topic for another day.

For now, lesson learned.

Don’t. Run. Out. Of. Money.

Until next week,

— Jonah 🧱

P.S. Want to connect? Find me on LinkedIn and my projects on Instagram.